Artículo

Introduction

My favorite restaurant growing up was a Utah favorite: Café Rio. Every time you visited, the employees were happy, and they did the chant “Extra Meat” anytime someone added to their burrito. They had napkins that were thicker and softer, stacked in a criss-cross pattern that was aesthetically appealing and made it easy to grab the perfect amount for your table. In ten years of eating there, I never had a single bad experience.

In 2017, Café Rio was acquired. What was once a weekly stop for my family has become a place that reminds me how not to treat customers. The food has declined significantly, and the customer service is abysmal. The criss-cross napkins are gone. Nobody does the chant.

There was a time when additional capital and larger partners were often a net positive for the companies. I think most of us have recently experienced the downside of those systems, particularly in hospitality.

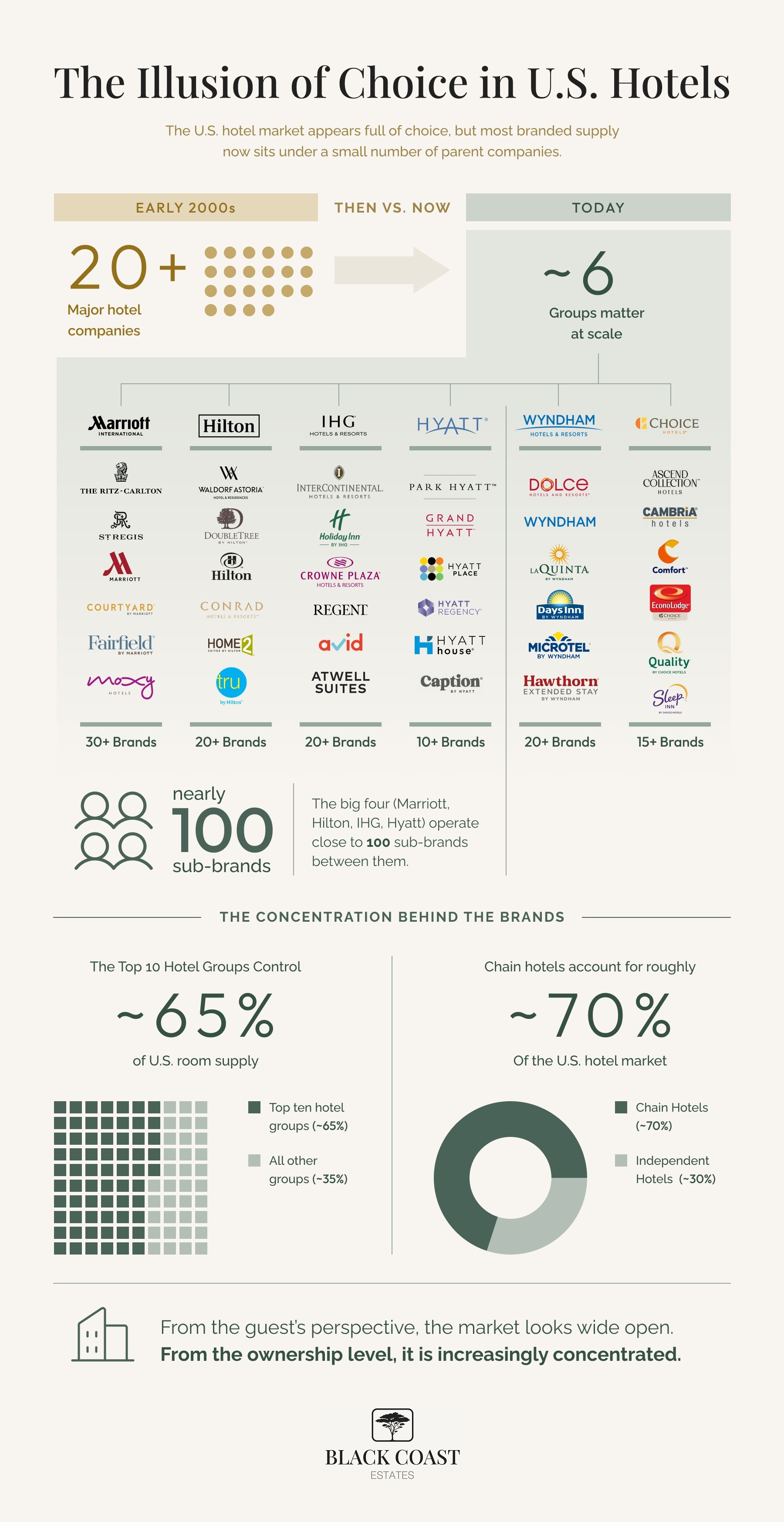

The Quiet Concentration of Hospitality

The hotel industry is far more concentrated than it looks. In the early 2000s, more than twenty major hotel companies competed in the United States. Today the field has collapsed to roughly half a dozen names that matter at scale (Marriott, Hilton, IHG, Hyatt, Wyndham, and Choice), with the ten largest groups controlling about 65% of U.S. room supply. Chain hotels make up roughly 70% of the overall U.S. market. Between them, the big four operate close to 100 sub-brands.

That consolidation is hidden by design. Walk any airport terminal, any interstate exit, any "up-and-coming" downtown, and the lobbies look different: different fonts, different lighting packages, different signature scents. But the ownership chart behind them keeps narrowing. A traveler choosing between four "different" hotels on the same block is often choosing between four brands owned by the same parent.

Restaurants tell a quieter version of the same story. A beloved local concept gets bought, scaled to forty locations, and quietly hollowed out. The things that made regulars regulars are the first line items to go. The chant, the criss-cross napkins, the line cook who actually likes you (none of it survives contact with a corporate operations manual). Moody’s has been downgrading the debt of PE-owned chains for years; the regulars notice the food first.

The mechanism is not mysterious. Scale rewards what can be standardized and punishes what cannot. A napkin fold is unmeasurable on a P&L. “Extra Meat” does not show up in a labor model. So the things that made a place worth loving are the first to get cut, and the things that load cleanly into a spreadsheet (unit count, ticket time, food cost percentage) are what survive.

The Question Worth Asking

Isaac French said something that hit me to my core:

“Maybe the question we should be asking ourselves is not if hospitality can scale, but if it should.”

Scale is not neutral. Every choice to grow is a choice about which details survive contact with a corporate style guide and which ones don’t. A founder who personally laid out the napkin pattern can defend it. A regional ops director two acquisitions removed from that founder cannot, and won't, because the napkin pattern is not in the brand standards binder.

What We’re Building at Black Coast

Our goal at Black Coast is to embody this principle. We are completely dedicated to building a project where people not only own a vacation home they love, but where the details handled by management amplify the experience rather than flatten it. The napkin pattern matters. The chant matters. Whether the person checking you in actually remembers your name matters.